A genuine buyer cannot be deprived of Input Tax Credit and instead recovery action should be taken against the defaulting supplier

ITC is ineligible where there is delay in filing GSTR 3B beyond the time limit prescribed under Section 16(4) of the CGST Act

Bombay HC allows benefit of Article 13(4) of India Singapore DTAA on capital gains and rejects Revenue’s contention on application of Article 24 (Limitation of Relief)

Delhi HC: No error committed by Tribunal in law or in facts by following APA approach for non covered years

Indirect acquisition of shares of Target Company through share transfer in promoter entity triggers open offer obligations

ITAT allows long term capital loss on intra group share transfer claimed through revised return

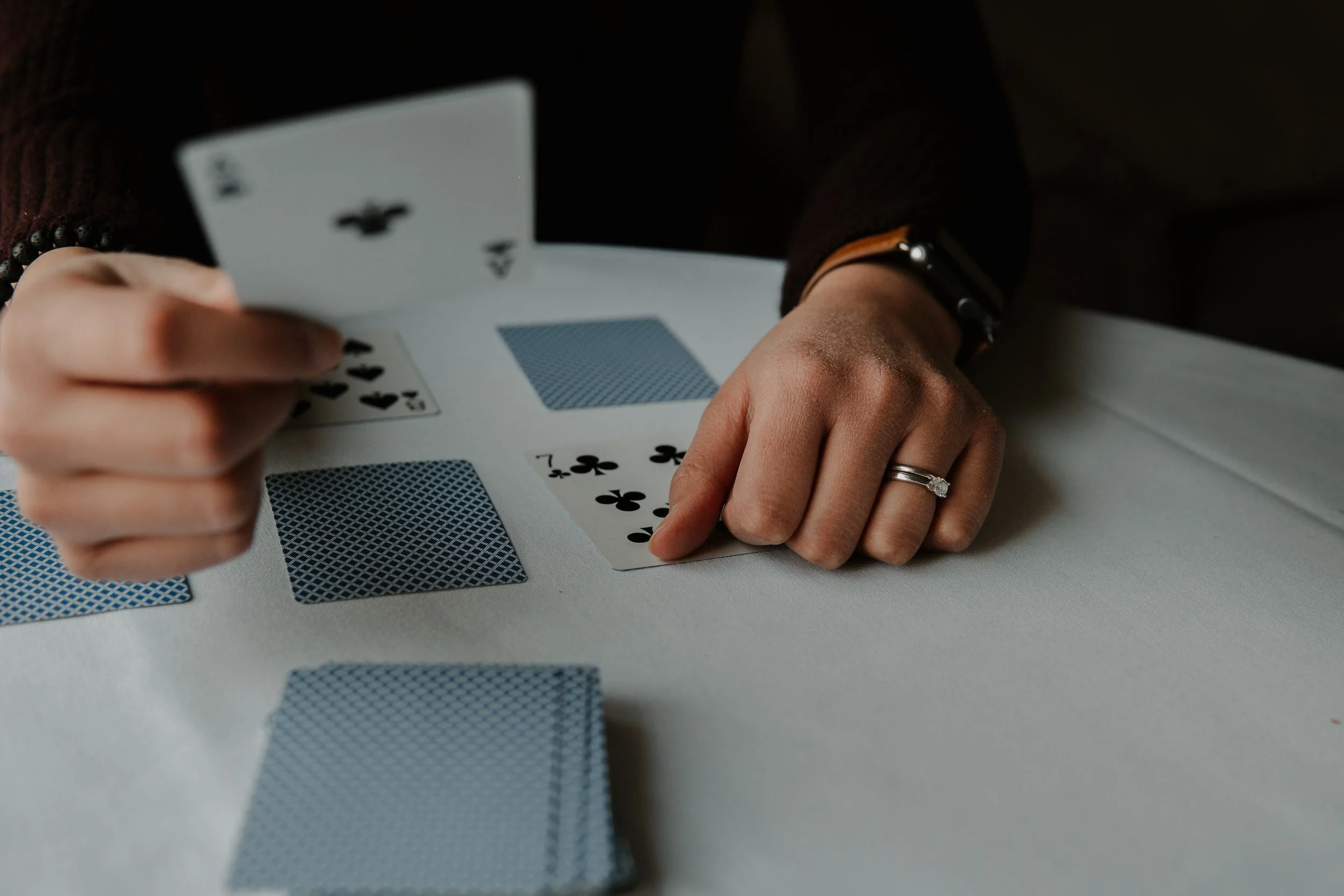

Entry 6 of Schedule III of the CGST Act provides that lottery, betting, and gambling are subject to GST, while other actionable claims are not.

Section 56(2)(viia) would prevail over section 47(vi) for shares transferred on account of amalgamation